There’s no doubting that 2020 was a tough ride for the insurance industry. With 2021 shaping up to be perhaps just marginally better, many industry executives are concerned about their organizations ability to adapt.

In a recent Deloitte survey, very nearly half of executives agreed that the Covid pandemic “showed how unprepared our business was to weather this economic storm”.

As a result, many providers are ramping up existing automation projects aimed at reducing costs and increasing efficiency.

But automation is a broad discipline. Businesses in every sector struggle to define what precisely their requirements are, let alone which products would meet them.

It’s a tyranny of choice; an increasingly accessible automation industry offers many options, and heightens the fear of choosing the wrong one.

In this post we’re going to focus on the automatable steps behind a single, common insurance process; First Notification of Loss (FNoL). What we’ll learn from this test case can be applied to virtually any routine process.

In this post:

- Establishing caller intent

- Authenticating the caller

- Gathering and confirming customer data

- Handing over to the agent

Establishing caller intent

Any customer conversation begins by establishing the customer’s need. This is generally known as ‘capturing intent’ and is relatively simple to handle with automated conversational tools.

Conversational AI is an increasingly common tool that enables customers to communicate their need with natural language. Unlike traditional IVR systems, which are limited in scope, a conversational system can process a wide range of inputs.

One speech recognition case study found that the automated system was able to capture intent fully in 75% of cases.

In our FNoL example, a customer would likely use a phrase like ‘I need to make a claim’ or ‘I’ve been in an accident’. Modern natural language systems understand both the specific words the customer uses and the underlying intent.

This is the first step, triggering the series of actions you’ve defined for your FNoL process.

There are two major advantages to automating this stage of the customer journey:

- The process of collecting and processing data is underway before the caller reaches a human agent. That’s useful, especially when you consider that insurance agents spend 30-40% of their time documenting interactions.

- Other, less pressing queries can be handled entirely by the automated conversational system. For example, a simple request for information doesn’t need agent intervention at all.

Conversational tools like Alexa have made customers far more willing to engage with similar tools in service. babelforce implementations have seen as many as 60% of customers opt for conversational AI as their first choice.

Authenticating the caller

Most businesses choose to place this step after capturing intent as many interaction types do not require authentication.

Automation does more than just save time here; authentication often involves personal or protected information which contact centers do not want to record. Automating this step removes the need to ‘plan around’ call recording.

There are several forms that automated authentication can take. Again, conversational tools may have a role; it’s also true that customers often prefer dialpad input (DTMF) for information such as personal reference numbers.

Computer Telephony Integration (CTI) is a vital addition here. While CTI is essentially a default for most business’s customer support, few make full use of its capabilities. For example, CTI enables your organization to ‘recognize’ incoming callers based on the number they’re dialing from.

That can form a provisional stage of authentication. Additionally, it can help you to guide customers who already have a query in progress. For example, Delta Air Lines recognize callers and automatically present them with an overview of their bookings. This simple action keeps thousands of calls per year in self-service.

Gathering and confirming customer data

The next step is to gather details related to the claim. This stage is highly specific to each business and each claim but will include at minimum the time, location and nature of the claim.

Conversational AI fulfills this need as the caller needs only answer direct questions using natural language.

The bigger challenge is to confirm this information with the customer – ideally in writing. One successful approach is to send the customer an SMS or email which they can check and confirm – or amend – during this stage of the call.

Handling the process this way eliminates any potential for misunderstanding between the customer and the automated system. The claim can proceed with an account that’s agreed between your business and your customer.

It also enables your human agent to begin their portion of the call armed with all the relevant details. Their job is the part that only a human can do; understanding the deeper context and supporting the customer empathetically.

But the early stages of the claim – including data gathering – are more effective when automated. Thoughtfully applied automation has been shown to reduce the cost of a claims journey by as much as 30%.

Handing over to the agent

The final stage is the handover to the agent. In this part of the interaction there are three key considerations:

#1 Hand over to the *right* agent

Intelligent routing ensures that each caller reaches the right agent based on the information they’ve provided. This is generally related to agent skill sets including claims type, urgency and fraud detection.

An effective call routing platform makes this as simple as possible; managers ‘tag’ agents with skill sets at the push of a button. The tagged skills align with call types.

#2 Provide the agent with all available information

A simple screen-pop means that the agent can review the details of a claim before the customer reaches them. That’s an important feature of excellent customer service; as much as 75% of a typical phone conversation is not ‘conversation’ at all. It’s comprised of manual research and systems navigation.

#3 Offer alternatives when agents are unavailable

If there are no agents available to handle this portion of the call, you’ll need to provide an alternative service. This will usually be a scheduled outbound call to the customer, or virtual queuing system.

Automated outbound dialing and queuing – AKA virtual queuing – is an option that three-quarters of customers opt for.

What should the insurance industry learn?

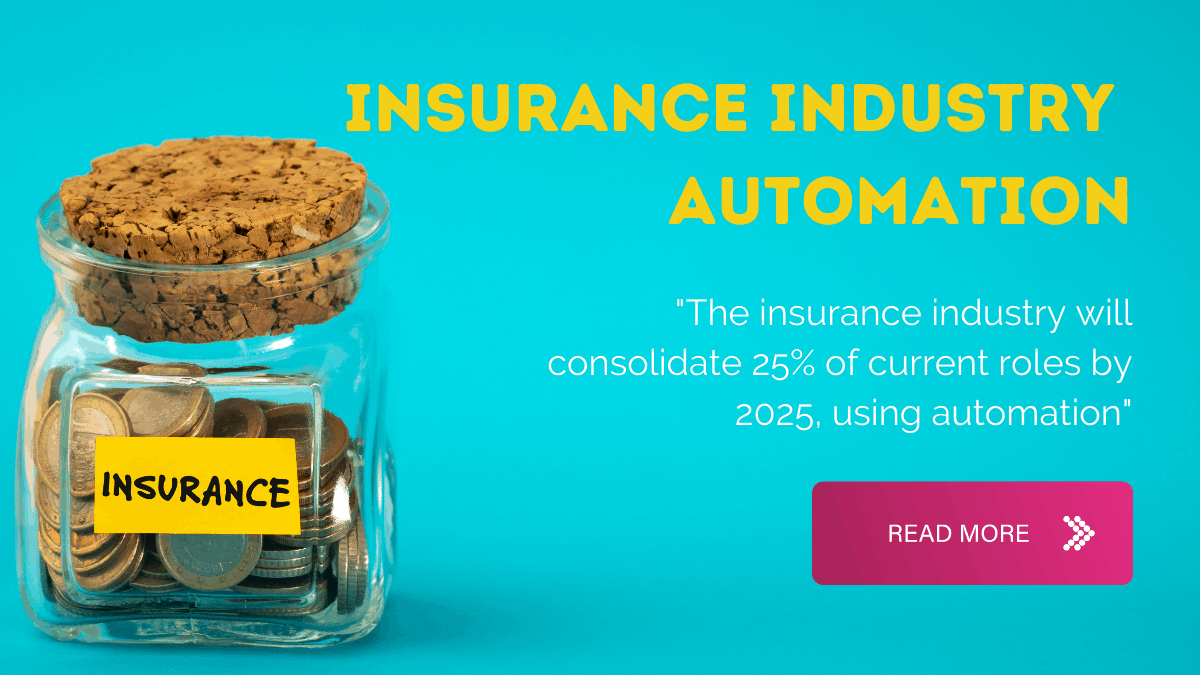

Research from McKinsey indicates that the insurance industry will reduce or consolidate 25% of current roles by 2025, using automation.

It’s a process that begins with the automation of relatively simple tasks. Any dedicated business can achieve what we’ve discussed quite easily but no single element radically alters a business’s customer experience.

Instead, it’s the combination of numerous automated contact handling processes that lead to faster, cheaper and more efficient service.

It’s an approach that babelforce handles for businesses in insurance and other sectors on a daily basis.

Our No-Code automation platform makes it easy to conceptualize and deploy automated processes within any customer journey and across any contact channel – including each we’ve discussed today.

To find out more, download your free contact center automation eBook now.